Health Insurance Claim Rejection in India is more common than most people realize. Ramesh thought he had done everything right. For three years, he paid all his health insurance premiums on time. जब उसकी emergency heart surgery हुई, उसने उम्मीद की कि उसका ₹3 लाख का खर्चा कंपनी उठा लेगी। लेकिन अस्पताल से निकलने के बाद, उसे एक झटका लगा—claim मिला ‘rejected’, क्यूंकि उसने hypertension (high BP) छुपाया था।

यह सिर्फ़ Ramesh की कहानी नहीं है। IRDAI (Insurance Regulatory and Development Authority of India) के FY 2023-24 के data के अनुसार, health insurers ने ₹26,000 crores की claims reject की हैं। यानी, हर 10 में से 1 health claim reject हो गया! 43% policyholders ने report किया कि उन्हें अपना claim process करवाने में बड़ी परेशानियाँ आई।

अगर आप end तक पढ़ेंगे, आपको समझ आएगा कि health insurance claim reject क्यों होते हैं—and steps कैसे लें जिससे आपका claim reject ना हो।

5 Common Reasons for Health Insurance Claim Rejection in India | 5 आम कारण

आप इन handy links का इस्तेमाल करके article में जल्दी से navigate कर सकते हैं:

1. Incomplete / Wrong Documentation in Health Insurance Claim Rejection | अधूरी या गलत डॉक्यूमेंटेशन

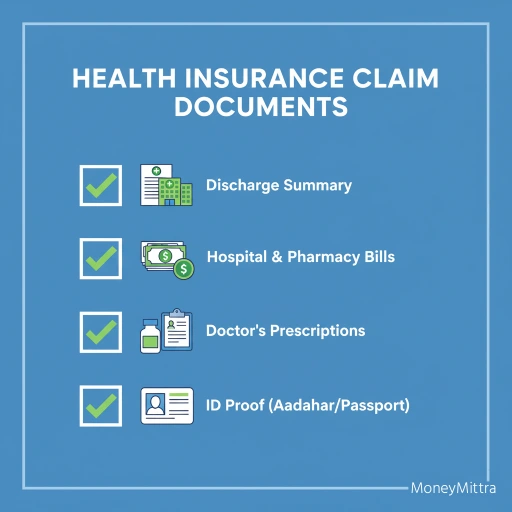

Health insurance claim rejections due to documentation issues are one of the leading causes of denied claims in India. Insurance companies are extremely particular about documentation accuracy and completeness, as even minor errors can lead to automatic rejections।

Discharge Summary की कमियां

जब हम health insurance claim करते हैं, तो सबसे महत्वपूर्ण दस्तावेज़ों में से एक होता है Discharge Summary। यह अस्पताल से मिलने वाला वह पेपर होता है जिसमें आपके पूरे इलाज का सारांश लिखा जाता है—admission date, discharge date, diagnosis, treatment details, दवाइयां और डॉक्टर की observations।

लेकिन कई बार इसी discharge summary में कमियां रह जाती हैं और यही health insurance claim rejection का कारण बन जाता है।

- अगर hospital seal या stamp नहीं लगी हो तो document invalid माना जाता है।

- Medical details अधूरी हों—जैसे diagnosis साफ़ न लिखा हो, treatment duration mention न किया गया हो, या दवाइयों के बारे में पूरी जानकारी न दी गई हो—तो claim reject हो सकता है।

- Admission और discharge की dates में mismatch होने पर भी insurer claim accept नहीं करता।

इसलिए ज़रूरी है कि discharge summary को ध्यान से check करें। Hospital से discharge होते समय यह verify कर लें कि सारी details पूरी और सही हैं। अगर कोई गलती दिखे, तो उसी समय correction करवाना सबसे अच्छा है।

याद रखिए, discharge summary एक official proof होती है कि आपने इलाज कराया है। छोटी सी चूक भी आपके claim को हफ्तों या महीनों तक delay कर सकती है।

Claim Form की त्रुटियां

जब भी health insurance claim की बात आती है, सबसे पहली और सबसे अहम चीज़ होती है Claim Form। यह छोटा-सा form आपके पूरे इलाज और खर्च की कहानी insurance company तक पहुँचाता है। लेकिन यहीं सबसे ज़्यादा गलतियां होती हैं। मैंने कई बार लोगों को देखा है कि genuine treatment के बाद भी उनका claim reject हो गया, सिर्फ इस form की छोटी-सी चूक की वजह से।

आइए जानते हैं कि Claim Form में कौन-कौन सी गलतियां सबसे आम हैं।

- मेरे एक दोस्त ने दावा (claim) किया था। सबकुछ genuine था, लेकिन उसने policy number में एक digit गलत लिख दी। System ने तुरंत इसे mismatch मान लिया और claim reject कर दिया।

- बहुत बार देखा है कि लोग जल्दी-जल्दी में नाम की spelling गलत लिख देते हैं, या Date of Birth (DOB) match नहीं करते। Insurance company को यह शक होता है कि कहीं fraud तो नहीं हो रहा।

- मेरे एक relative का case याद आता है—उन्होंने सिर्फ कुल खर्च ₹80,000 form में लिखा। लेकिन detailed breakup (room rent, OT charges, medicines) नहीं डाला। Insurer ने verification रोक दी और extra documents मांगे। Claim 2 महीने delay हुआ।

- यह सबसे common है। कई लोग form submit करते वक्त signature करना भूल जाते हैं। बिना sign के form invalid हो जाता है। एक बार मेरे जानने वाले को सिर्फ इस वजह से फिर से पूरा process दोहराना पड़ा।

Hospital Bills और Reports की समस्याएं

Health insurance claim approval का सबसे बड़ा आधार होता है Hospital Bills और Medical Reports। Insurance company इन्हें देखकर verify करती है कि इलाज वास्तव में हुआ है और खर्च genuine है। लेकिन छोटी-सी लापरवाही भी आपके claim को reject कर सकती है।

आइए जानते हैं hospital bills और reports से जुड़ी वे common mistakes जिनके कारण claim delay या reject हो सकता है।

- कई लोग hospital से सिर्फ कुल खर्च वाला bill लेते हैं। लेकिन insurance companies को detailed breakup चाहिए—room rent, operation theatre charges, nursing charges, consultation fees, pathology charges आदि।अगर breakup नहीं होगा, तो insurer को doubt होता है और claim रोक दिया जाता है।

- Original hospital bills पर proper bill number होना ज़रूरी है। बिना bill number के document fake या duplicate माना जा सकता है।Example: अगर आपने ₹1,20,000 का bill दिया लेकिन उस पर serial number या invoice number नहीं है, तो insurer उसे valid proof नहीं मानेगा।

- Insurance company सिर्फ bills से संतुष्ट नहीं होती। वे lab reports, X-rays, CT scans, pathology reports भी verify करते हैं। अगर इनमें से कोई report missing है, तो claim incomplete माना जाता है।

- Doctor की prescription medical necessity का सबसे बड़ा proof है। अगर prescription में medicine का नाम, dosage या duration mention नहीं है, तो insurer यह मान सकता है कि खर्च genuine नहीं है।

Original vs Photocopy की समस्या

Health insurance claim process में सबसे ज़्यादा confusion होती है कि insurer को original documents चाहिए या photocopy चलेगी। कई बार लोग यह समझ नहीं पाते और इसी छोटी-सी गलती की वजह से claim delay या reject हो जाता है।

आइए समझते हैं कि insurance companies documentation को लेकर इतनी strict क्यों होती हैं और आपको किन बातों का ध्यान रखना चाहिए।

- अधिकतर insurance companies original hospital bills, discharge summary और investigation reports मांगती हैं। Reason यह है कि insurer को यह proof चाहिए कि treatment वाकई हुआ है और खर्च genuine है।

अगर आप सिर्फ photocopy जमा करेंगे, तो claim almost निश्चित रूप से reject हो सकता है। - कुछ cases में insurers photocopies accept कर लेते हैं, लेकिन condition होती है कि वे properly attested (verified with stamp/signature) हों। Problem तब होती है जब लोग बिना attestation के simple photocopy जमा कर देते हैं।

Insurer ऐसे documents को invalid मान लेता है और claim रोक देता है। - आजकल कई लोग सिर्फ digital scanned copies submit करते हैं। जबकि कई insurers अभी भी physical hard copies demand करते हैं। अगर आपने सिर्फ email से digital files भेज दीं और physical originals नहीं दिए, तो आपका claim incomplete मान लिया जाएगा।

अन्य महत्वपूर्ण Documentation Issues

- Health insurance claim process में अक्सर rejection की सबसे बड़ी वजह होती है documentation errors और form filling mistakes। कई लोग सोचते हैं कि सिर्फ इलाज होना या hospital bills देना काफी है, लेकिन insurance company हर detail verify करती है।

- सबसे पहली category है Identity और Policy Verification। अक्सर claim reject इसलिए हो जाता है क्योंकि ID proof, जैसे Aadhaar या PAN card, policy details से match नहीं करते। कई लोग original policy document submit करना भूल जाते हैं या health card/TPA card की copy नहीं देते। इन छोटी-छोटी गलतियों के कारण insurer को claim approve करने में दिक्कत होती है।

- दूसरी category है Payment और Bank Details। Reimbursement के लिए cancelled cheque या NEFT form submit करना ज़रूरी होता है। कई बार NEFT form incomplete होता है या account number policy में registered account से अलग होता है। ऐसी समस्याओं की वजह से claim rejection या delay हो सकता है।

- Emergency और Accident Cases में documentation और timing critical होती है। Accident होने पर FIR submit करना भूलना, Medico Legal Certificate (MLC) नहीं देना या claim notification में देरी करना (24–48 hours rule) rejection की आम वजहें हैं।

- Pre-authorization Issues भी अक्सर लोगों को confuse करती हैं। Planned surgeries के लिए pre-approval नहीं लेना, hospital या doctor registration numbers नहीं देना, या non-network hospital में treatment के proper documents ना होना claim reject करने के कारण बन सकता है।

- Supporting Documents की कमी भी बड़ी समस्या है। Pharmacy bills incomplete होना, doctor consultation receipts नहीं देना, pathology या radiology reports missing होना, या expensive procedures में implant/device bills न देना अक्सर claim delay या reject करते हैं।

- Form filling में भी common mistakes होती हैं। Handwriting illegible होना, form के कुछ sections incomplete छोड़ देना, wrong claim category select करना (cashless या reimbursement) या date format गलत होना claim process को slow या reject कर सकता है।

Example: एक मामले में नाम गलत होने की वजह से ₹50,000 का claim reject हुआ और सही कागजात देने में 1 महीना extra लग गया। इसे avoid करने के लिए, अपने सभी details जैसे नाम, policy number, hospital bills सही रखें। सारे originals संभालकर रखें और copies अपने पास रखें। documents को organized रखें—admission papers, reports और bills अलग-अलग रखना आसान बनाता है।

2. Pre-Existing Diseases and Health Insurance Claim Rejection in India | पहले से बीमारी छुपाना

Health insurance claims rejection का सबसे बड़ा कारण होता है pre-existing diseases को disclose न करना। Insurance Regulatory and Development Authority of India (IRDAI) के अनुसार, FY 2023-24 में insurers ने कुल ₹15,100 करोड़ के claims reject किए, जो filed claims का लगभग 12.9% था। इन rejected claims में लगभग 12% cases सिर्फ इसलिए थे क्योंकि policyholder ने पहले से मौजूद बीमारी (pre-existing condition) को छुपाया था।

FY 2023-24 के आंकड़े यह दिखाते हैं कि कुल health insurance claims लगभग ₹1.17 लाख करोड़ थे, जिनमें से ₹15,100 करोड़ claims reject किए गए। कुल 3.26 करोड़ claims process हुए और 2.69 करोड़ claims settle किए गए, जिससे 82.46% settlement rate पाया गया। इन आंकड़ों से स्पष्ट है कि pre-existing disease का non-disclosure insurance claim rejection का एक महत्वपूर्ण कारण है।

अगर आप pre-existing conditions disclose नहीं करते हैं, तो insurance company आपके treatment और hospitalization को non-genuine claim मान सकती है और claim reject कर सकती है। इस वजह से आपके genuine medical expenses भी reimbursement के लिए eligible नहीं रह जाते।

कुछ लोग अपने Diabetes, high blood pressure (BP), asthma या पिछले surgeries की जानकारी नहीं देते। कई बार पुराने hospital records, medications और doctor consultations को भी application में mention नहीं किया जाता। इसके अलावा, लोग अपने family medical history, जैसे आनुवंशिक बीमारियों का इतिहास भी छुपा देते हैं। कुछ cases में लोग जानबूझकर गलत जानकारी भी भर देते हैं, जिससे claim fraudulent माना जा सकता है।

Lifestyle diseases जैसे Diabetes mellitus, hypertension, obesity और thyroid disorders अक्सर undisclosed रहते हैं। Chronic conditions जैसे asthma, arthritis, kidney stones और महिलाओं में PCOD/PCOS भी कई बार छुपाई जाती हैं। Past surgeries, cardiac procedures, cancer treatment और accident-related treatments को भी कई लोग application में नहीं बताते।

Mental health issues जैसे depression, anxiety, psychiatric medications और counseling history को भी policyholders disclose नहीं करते। इन सभी non-disclosures की वजह से insurance company को लगता है कि claim incomplete या fraudulent हो सकता है, और claim reject हो जाता है।

इसलिए health insurance application भरते समय सभी pre-existing conditions और medical history पूरी ईमानदारी से disclose करना बहुत जरूरी है, ताकि आपके genuine treatment और hospitalization के लिए claim smooth approve हो सके।

Insurance Company की Investigation Process

Insurance company claim approve करने से पहले कई तरह की investigation process अपनाती है। सबसे पहले वे आपके medical records को verify करती हैं। Hospital database में पुराने admission records, pharmacy records और doctor consultation patterns की जांच की जाती है। इसके साथ ही आपके previous lab test reports को भी analysis के लिए लिया जाता है।

आजकल insurance companies digital footprint का भी इस्तेमाल करती हैं। Prescription uploads, online medicine orders, और health apps के data को track किया जाता है। Social media पर health-related posts की screening भी की जाती है और insurance database में previous policies के साथ cross-check करके verification किया जाता है।

Investigation की timeline भी structured होती है। Claim filing के तुरंत बाद immediate red flags को identify किया जाता है। IRDAI guidelines के अनुसार, insurance companies 48 महीने तक पीछे जाकर claim और medical history की जांच कर सकती हैं। Detailed medical underwriting के तहत आपकी पूरी medical history verify की जाती है और modern fraud detection algorithms जैसे AI-based pattern recognition का इस्तेमाल करके suspicious patterns detect किए जाते हैं।

इस process से insurers यह सुनिश्चित करते हैं कि claim genuine और accurate है। अगर कोई discrepancies पाई जाती हैं, तो claim reject या delay हो सकता है। इसलिए health insurance claim के लिए सभी documents सही, complete और transparent होना बहुत जरूरी है।

3. Delay in Claim Intimation: A Major Cause of Health Insurance Claim Rejection | समय से claim ना करना

Health insurance में claim intimation का समय पर करना बेहद महत्वपूर्ण होता है। IRDAI guidelines और insurance policies के अनुसार हर claim के लिए specific time limits होती हैं, जिनका पालन न करने पर claim rejection का जोखिम बढ़ जाता है।

Planned hospitalization के मामले में, policyholder को 48-72 घंटे पहले insurance company या TPA को advance intimation देना जरूरी होता है। अगर cashless facility चाहते हैं तो pre-authorization लेना आवश्यक है। साथ ही, written acknowledgment लेना और सभी medical documents और policy details ready रखना claim approval के लिए मददगार होता है।

Emergency hospitalization के लिए claim intimation की timing और भी critical होती है। IRDAI और insurance policies के अनुसार, 24 घंटे के अंदर insurer या TPA को inform करना चाहिए। कुछ policies में maximum 48 घंटे की छूट दी जाती है। Patient के परिवार की जिम्मेदारी होती है कि timely intimation करें और TPA के 24×7 toll-free helpline numbers का इस्तेमाल करें।

Reimbursement claims के लिए discharge के बाद claim filing की time limit 7-15 दिन होती है, जबकि document submission की maximum अवधि 30 दिन होती है। Complete documentation और properly filled तथा signed claim forms submit करना जरूरी है।

Recent IRDAI guidelines (2024) के अनुसार, turnaround time (TAT) को भी छोटा किया गया है। Cashless authorization अब 1 घंटे के अंदर approval या rejection के साथ होता है, final settlement discharge के 3 घंटे के अंदर possible है। Investigation cases में 45 दिन और non-investigation claims में 15 दिन के भीतर settlement होना चाहिए।

Delayed claim intimation पर insurers को penalties का सामना करना पड़ता है। IRDAI के नियमों के अनुसार delayed settlements पर bank rate + 2% interest देना अनिवार्य होता है। Hospital charges में हुई बढ़ोतरी insurer को bear करनी पड़ती है, और ombudsman awards implement न करने पर ₹5,000 daily penalty लग सकती है।

Common intimation problems में technical delays, गलत contact numbers, system downtime, incomplete documentation और communication barriers शामिल हैं। Emergency situations में family का focus treatment पर होना, out-of-station treatment, weekend/holiday issues या ICU/critical care में patient unconscious होना intimation को delay कर सकता है। Policy awareness issues जैसे exact time limits का knowledge न होना, missing contact details, multiple policies का confusion और intimation procedure ignorance भी अक्सर claim delays का कारण बनते हैं।

Case studies से पता चलता है कि late intimation के कारण ₹2 लाख के claims reject हुए हैं। Weekend admissions में Monday inform करने पर rejection हुए और wrong channel से intimation करने पर भी processing delay हुई। वहीं, IRDAI intervention और consumer forum orders ने unavoidable circumstances और medical emergency में reasonable delays को accept किया, और technical delays के लिए insurer penalties लागू की।

इसलिए, health insurance claim की approval सुनिश्चित करने के लिए समय पर intimation करना, documentation complete रखना और insurer/TPA से proper communication करना बेहद जरूरी है। Timely intimation से न केवल claim approval की chances बढ़ती हैं बल्कि unnecessary delays और financial stress भी कम होते हैं।

4. Policy Exclusions Leading to Health Insurance Claim Rejection in India | पॉलिसी एक्सक्लूजन

Health insurance policy लेने से पहले यह समझना बेहद जरूरी है कि हर policy में कुछ specific treatments और diseases cover नहीं होते, जिन्हें हम policy exclusions कहते हैं। यदि आप इन exclusions को ध्यान में नहीं रखते, तो आपका claim automatically reject हो सकता है। खासकर pre-existing conditions यानी ऐसी बीमारियाँ जो policy शुरू होने से पहले मौजूद थीं, उन्हें सामान्य तौर पर policy में cover नहीं किया जाता। इसके अलावा, कई policies में waiting period लागू होता है, जिसका मतलब है कि policy शुरू होने के बाद कुछ समय तक इन pre-existing बीमारियों का इलाज insurance coverage में शामिल नहीं होगा।

Dental treatments जैसे सामान्य दांत निकालना, root canal या cleaning भी अक्सर exclusions में आते हैं। Cosmetic procedures, जैसे ब्यूटी या cosmetic surgery, और template-based aesthetic treatments भी अधिकांश health policies में cover नहीं होते।

Maternity और newborn care के खर्चे, जिसमें pregnancy, delivery और नवजात शिशु की देखभाल शामिल है, कई policies में exclude होते हैं। Alternative therapies जैसे आयुर्वेद, होम्योपैथी, यूनानी या naturopathy भी कई insurers cover नहीं करते।

Obesity treatment और bariatric surgery जैसे मोटापा कम करने वाले उपचार, STDs और HIV/TB के इलाज, self-inflicted injuries यानी आत्महानि या खुद की चोटों के इलाज, और substance abuse जैसे शराब, नशा या ड्रग एडिक्शन के treatments भी exclusions में रखे जाते हैं।

कुछ policies में experimental treatments या नए therapies cover नहीं होते। Dental implants, orthodontics, braces, aligners, और certain hernia repair mesh या device costs भी कई बार exclusion list में होते हैं।

इसलिए, health insurance policy लेने से पहले exclusions की पूरी list ध्यान से पढ़ना और समझना बहुत जरूरी है। ऐसा करने से आप future में claim rejection से बच सकते हैं और अपने coverage की सीमाओं को स्पष्ट रूप से जान सकते हैं।

5. High Hospital Bill Disputes & TPA Issues in Health Insurance Claim Rejection | हॉस्पिटल बिल विवाद/TPA की परेशानियां

Health insurance claim process में hospital bills और TPA (Third Party Administrator) से जुड़ी समस्याएं आम हैं। कई बार policyholder को लगता है कि सबकुछ सही है, लेकिन claim approval में delay या rejection हो जाता है। इन समस्याओं से बचने के लिए proactive approach और proper documentation बेहद जरूरी है।

सबसे आम समस्याओं में approval में delay होना शामिल है। कभी-कभी hospital या TPA प्रक्रिया में समय लग जाता है, जिससे claim late process होता है। Hospital network confusion भी एक बड़ी वजह है; यदि patient non-network hospital में treatment करवा रहा है, तो authorization नहीं मिल सकता या cashless claim reject हो सकता है।

कई cases में arbitrary deductions होती हैं, यानी unnecessary itemized deductions या bill adjustments कर दिए जाते हैं। इसके अलावा, incomplete pre-authorization भी common issue है, जहां verbal approval मिलने के बावजूद cashless facility बाद में reject हो सकती है।

Transparency की कमी भी claim disputes का कारण बनती है। कभी-कभी TPA या hospital यह स्पष्ट नहीं करते कि deductions क्यों किए गए। इसके साथ ही, multiple follow-ups के बावजूद response नहीं मिलना और hospital-TPA के बीच coordination gap भी claim approval delay करता है।

कुछ technical issues भी देखने को मिलते हैं, जैसे bill coding errors, जिसमें procedure codes या diagnosis codes गलत होने के कारण claim reject हो सकता है। Non-medical items जैसे toiletries या newspapers भी कभी-कभी charge हो जाते हैं। Unapproved room category के लिए भी deductions की समस्या आती है, जब higher room category में admit होने पर insurer claim adjust करता है।

इन सभी disputes से बचने के लिए जरूरी है कि आप treatment और billing के दौरान proper documentation, itemized bills, pre-authorization approvals और TPA communication records संभालकर रखें। यह practice न केवल claim approval को smooth बनाती है, बल्कि unnecessary delays और financial stress से भी बचाती है।

Quick Checklist | फटाफट चेकलिस्ट

- अपनी health conditions हमेशा ईमानदारी से disclose करें, ताकि कोई pre-existing disease छुपने की वजह से claim reject न हो।

- सभी forms, bills, medical reports और personal details को double-check करें, ताकि कोई जानकारी गलत या अधूरी न रहे।

- अस्पताल में admit होते ही 24-48 घंटे के भीतर insurer या TPA को call या email करके सूचित करें, क्योंकि delay से claim process में परेशानी हो सकती है।

- अपनी policy के exclusions और waiting periods को ध्यान से पढ़ें और समझें कि कौन-सी treatments covered हैं और कौन-सी नहीं, और किसी बीमारी के लिए waiting period कितना है।

- सारे hospital bills, admission papers, medical reports और prescriptions एक file में organized रखें, ताकि claim जल्दी और आसानी से process हो सके।

- pre-authorization की जरूरत होने पर इसे पहले से सुनिश्चित करें और approval documents संभालकर रखें।

- cashless facility का लाभ लेने के लिए अपने insurer के network hospitals में ही treatment करवाएं।

- policy terms और conditions को अच्छे से पढ़ें, ताकि किसी clause की वजह से claim reject या delay न हो।

- documentation में कोई भी missing information या incorrect entry नहीं होनी चाहिए, इससे multiple follow-ups और delays बचेंगे।

- insurer या TPA के साथ communication records (calls, emails) सुरक्षित रखें ताकि किसी dispute की स्थिति में प्रमाण के रूप में काम आए।

IRDAI (Insurance Regulatory and Development Authority of India)और industry reports के मुताबिक़ 2023-24 में लगभग 71% claims approve हुए, लेकिन high-value claims पर ज्यादा scrutiny होती है। डॉ. गिरधर ग्यानी (AHPI) बताते हैं कि delays अक्सर insurer और TPA (Third Party Administrator.) के multiple approvals की वजह से होते हैं, और seamless digital process से rejections कम किए जा सकते हैं। ध्यान रहे, यह जानकारी केवल educational purpose के लिए है; insurance खरीदने या claim करने से पहले certified advisor या insurance agent से सलाह लेना जरूरी है।

Disclaimer: यह ब्लॉग केवल educational purpose के लिए है। Insurance खरीदने या claim करने से पहले certified advisor/insurance agent से सलाह लें।

Conclusion

Your health is priceless—अपने परिवार और भविष्य के लिए अभी सावधान रहें।

Don’t let paperwork or technicalities steal your peace of mind.

Download our free Health Insurance Claim Checklist (PDF) to stay protected

या

Compare best insurance plans now

Internal Link: How to Choose Best Health Insurance in India

External Links: IRDAI | National Health Authority | Insurance Ombudsman